Pfizer Stock: Finally, A Dividend Stock Worth Buying (NYSE:PFE)

[ad_1]

JuSun

Introduction

I’ve written a lot about how overvalued dividend stocks have been during the past 4 years. Other than a brief period in March 2020, when a few good higher-yield stocks were trading at attractive valuations, the massive influx of Baby Boomers going into retirement combined with a decade of low bond yields pushed many investors into stocks who were seeking income from dividends. While most dividend stocks are still in a bubble, there is one that has been left for dead by investors: Pfizer (NYSE:PFE). It’s the first quality high-yield stock I’ve been able to find trading at a good valuation since I suggested buying Valero (VLO) on October 8th, 2020 in my article « The Cycle Will Turn Up. Valero Is A Buy » over 3 years ago. At the time, Valero’s dividend yield was over 9%. I have since taken profits, but Valero’s total return since then has been about +250%.

Pfizer’s situation is different than Valero’s, and Pfizer is not as easy of a call, but if an investor is looking for a good yield, with at least some opportunity for growth down the road, Pfizer is a decent bet over the medium term. In this article, I will take investors through my « Dividend Time-Until-Payback » analysis which is the process I use specifically when focusing on stock dividends. I will also explain why I think this type of analysis works reasonably well for Pfizer stock.

Checking Pfizer’s Earnings History

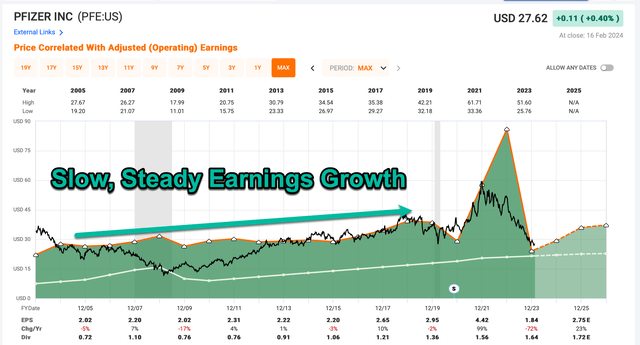

The first thing I check with any stock is what sort of earnings history it has. Because earnings patterns often repeat, the earnings history will help me determine what type of business and stock Pfizer is, which will let me know what type of analytical technique is best to use for the stock.

FAST Graphs

In the FAST Graph above we can see that pre-COVID, Pfizer had very slow, but very steady earnings growth, which picked up a little bit around 2016. During COVID Pfizer experienced a predictable boom/bust from supplying the world with vaccines. Smart investors understood that 2021 and 2022 earnings growth wouldn’t last because these vaccine sales were part of a temporary « boom », just as smart investors now should understand the overproduction of vaccines in 2023 and the earnings decline that followed likely won’t last as well. The most probable outcome is that Pfizer returns to similar earnings levels experienced before the pandemic over the next year or two. And, that is what Wall Street analysts currently expect as well with EPS rising to $2.75 per share in 2025, which is almost the same as the $2.95 they earned in 2019 pre-pandemic.

Because earnings have been so volatile during the boom/bust, much like a cyclical business (which is what my investing group The Cyclical Investor’s Club specializes in) recent earnings trends are not very useful for valuing the stock. Because of that earnings volatility, I am going to mostly focus on the dividend because it is much steadier and reflects what sort of earnings management thinks it can maintain over the longer term.

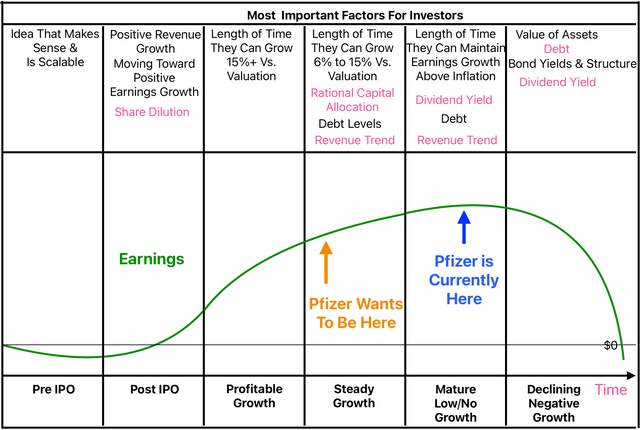

Pfizer’s Business Life Cycle Stage

Every successful public business has a life cycle. Along with earnings cyclicality, it is important to estimate early on in an analysis what part of the business life cycle a business is likely in, and where it’s trending toward over the medium-term future. I created the graphic below to help illustrate where I think Pfizer’s business belongs in this cycle.

The Cyclical Investor’s Club

Pfizer is a fully mature company currently in the stage of growth where the goal of the business is to maintain earnings growth above the rate of inflation while returning money to shareholders in the form of a dividend. We should expect a business in this stage of its life cycle to have a dividend yield in the 6% to 8% range if the stock is trading at a reasonable valuation. Pfizer’s yield is currently 6.08%, so it checks that box. The general thesis of owning the stock of a business at this stage of the cycle is that investors will be able to collect enough money from the dividend to get a good return before Pfizer’s business declines. Collecting that dividend is important because the stock price will almost always fall along with the eventual earnings decline whenever it comes. This creates a situation where the dividend of a mature company is basically in a race against time to return adequate money to shareholders before earnings can no longer keep up with inflation, which is why my « Time Until Payback » analysis focuses on time.

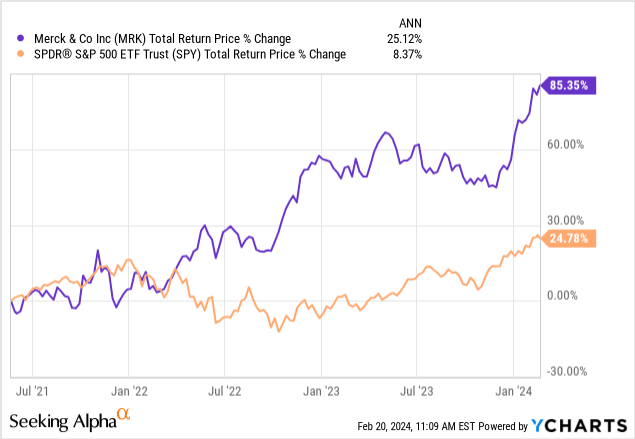

What I find most interesting about Pfizer’s situation, though, is that big pharmaceutical companies, due to patent expirations and things of that sort, are always investing in research and development or buying smaller businesses that have promising pipelines for new drugs. If they are successful in doing this, it is much easier for a big pharma business to actually travel backward along this business life cycle scale to return to a « Steady Growth » stage business (or if they are really lucky an even faster « Profitable Growth » stage business). This reversal in stages is much more difficult for other types of businesses that aren’t always prepared to constantly reinvent themselves. I pointed this out in my Merck (MRK) buy article « Merck Is A Great Relative Value & Good Absolute Value » article on May 22nd, 2021. After a long period of multiple compression and slow earnings growth, Merck then effectively traveled back to an earlier stage of faster growth via their success with Keytruda. The results since that article was published have been very good.

So, when a pharma company can not only delay the decline of its business but go back to an earlier stage of growth, it can be very lucrative for investors if the market allows them to buy at the right price. This is even better for dividend investors because the higher-than-average yields can potentially be paid out much farther into the future if things go well.

Pfizer’s Historical Earnings Growth

It’s a little counterintuitive for some, but dividend analyses should never start with the dividend and dividend yield. In fact, it’s possible to do a dividend analysis on a stock that doesn’t even pay a dividend. All an investor has to do is make some reasonable assumptions about what future dividends might be. Personally, I lean more heavily on history to guide my expectations of the future because I have found that’s the most reliable baseline to form expectations around.

All sustainable dividends come from earnings so examining earnings is the most reliable way to forecast long-term dividends. We can look at a business’s historical earnings growth rate and estimate what sort of long-term dividend outcomes are likely, and also get a sense of management’s preferred capital allocation and whether it makes sense.

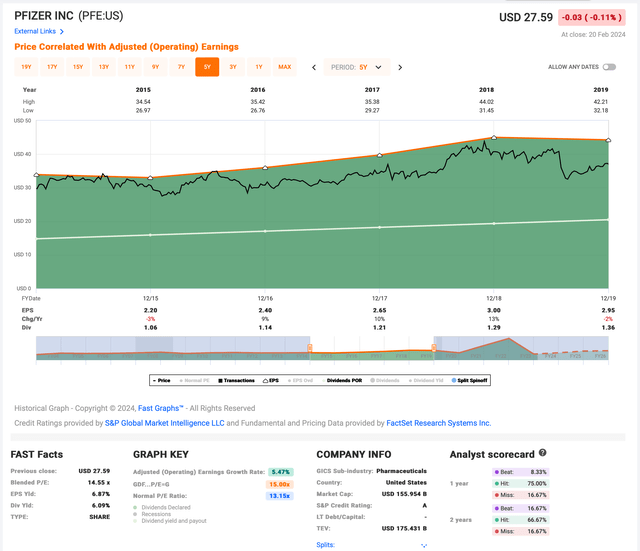

FAST Graphs

Above is a FAST Graph from the 5-year period before the COVID era. FAST Graphs has the earnings growth during this period at +5.47%, but I like to take into account the two modest down years of earnings growth in 2015 and 2019, so my estimate of earnings growth is just a little bit lower at +5.22%.

My assumptions here are that when the COVID dust settles over the next year or two, it is reasonable to expect 1) Pfizer’s earnings to return somewhere close to 2019 levels, plus, perhaps another 20-25% for inflation, and 2) for earnings growth to be in that 5% to 6% range after that.

This earnings growth rate matters because in order for dividends to grow sustainably over the long term, earnings have to grow first. Any dividend growth rate assumption will be bounded at some point by the earnings growth.

Pfizer’s Dividend Growth Expectations

I use a combination of 3 factors to estimate dividend growth. The first is the historical dividend growth rate, the second is my earnings growth estimate, and the third is the payout ratio. If the payout ratio is less than 50%, then I average the dividend growth rate and earnings growth rate together. This is because when the payout ratio is small, dividends can grow faster than earnings for some period of time before they need to slow down to be more in line with earnings growth. If the payout ratio is more than 50% I limit any dividend growth rate assumptions to my expected earnings growth rate. Unless we expect Pfizer’s earnings per share to bounce back above $3.44 per share near-term (which I do not) then the payout ratio will be above 50%. That means I will use the +5.22% earnings growth rate as my expected dividend growth rate instead of the 9-year compounded dividend growth rate of +5.84%, or an average of the two.

How Dividend Time Until Payback Works

Many investors prefer to focus on dividends and mostly ignore stock price volatility, and sometimes even ignore earnings volatility. While most of the time I don’t think that’s the most rational or optimal approach to stock investing, in Pfizer’s case, because both the earnings and stock price have been incredibly volatile due to the COVID boom/bust, using the dividend as a guidepost can be useful. The Dividend Time Until Payback analysis asks the simple question of how long it is likely to take to earn one’s initial investment in a stock back via only the collection of the dividend. Obviously, the shorter the time it takes to earn an investment back, the better.

In order to calculate this we only need the dividend yield and the expected dividend growth rate. I’ve found it’s best to use a hypothetical $100 investment assumption and then calculate how long it would take to turn that $100 into $200 using only the dividend payments. I pull forward the first year’s dividend growth, so instead of a $6.10 dividend on a $100 investment, I start with $6.42 (6.10 + 5.22% growth). Below is a table containing the dividend payouts over time and the cumulative amount of dividends collected. Because many retirees often intend to spend their dividends, I never assume the dividends are reinvested.

| Year | Dividend | Cumulative Dividends |

| 1 | $6.42 | $6.42 |

| 2 | $6.75 | $13.17 |

| 3 | $7.11 |

$20.28 |

| 4 | $7.48 | $27.76 |

| 5 | $7.87 | $35.63 |

| 6 | $8.28 | $43.91 |

| 7 | $8.71 | $52.62 |

| 8 | $9.16 | $61.78 |

| 9 | $9.64 | $71.42 |

| 10 | $10.15 | $81.57 |

| 11 | $10.68 | $92.25 |

| 12 | $11.23 | $103.48 |

It would take about 12 years for an investor to earn their initial investment back via Pfizer’s dividend with my assumptions.

Obviously, each investor will have to decide what time threshold is adequate for them. Personally, mine is about 10 years instead of 12 so I would need to see Pfizer’s price get down to around $22.40 per share for my dividend investing threshold to be met. I’ve noticed over time, however, that I tend to have higher return thresholds than most investors, and this 12-year time until payback that doesn’t include some sort of stock price depreciation is essentially the best in the S&P 500 right now. So, Pfizer is one of the best relative dividend opportunities in the market.

Why I Bought Pfizer

I recently bought Pfizer stock based mostly on an expectation that earnings would likely recover over the next two years, and then after that, there was some chance that they could bring winning products to market. The dividend, in this case, serves as a form of insurance and return while I wait to see what happens. One of the more difficult things to do as a stock analyst is simply to admit what you don’t know. That’s an advantage I have as an independent analyst compared to someone employed by Wall Street. I don’t think I’ve ever read or heard a sell-side analyst say « I don’t know », « It’s too hard » or « There isn’t enough information to have an opinion » about a stock. When it’s your job to have an opinion and your job to know something about a business, you are basically forced to make something up and sound as convincing as possible whether you know or not.

I’m happy to say I have no idea whether Pfizer will be successful over the next 5 years. But they did just buy Seagen, so we can see they are making an effort. They could have chosen to simply buy back stock, which is what a lot of mature businesses do. We have also witnessed that Pfizer has the means to very quickly develop things like the COVID vaccines when many other pharma companies could not do it. While there is never any guarantee of a future breakthrough, we can see that the effort is being made on several fronts.

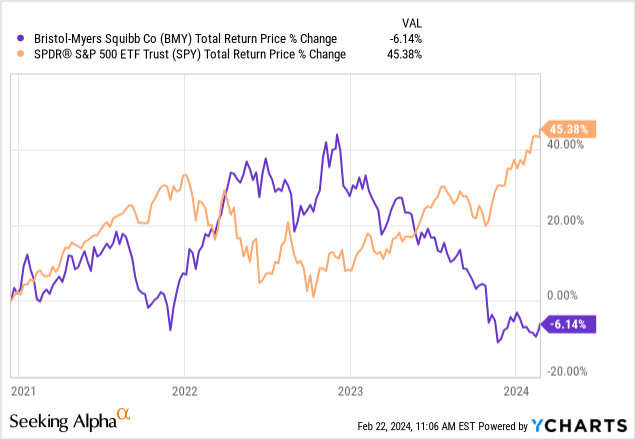

I mentioned Merck earlier as a model success story for this strategy. I also have a model of a less successful outcome (at least so far) of a similar approach, which Bristol-Myers Squibb (BMY), which I bought on 12/14/20. I probably paid a little too much for it compared to where Pfizer is, but nevertheless, BMY hasn’t done much in the past 3 years for me.

While it certainly had a period of good performance, overall, the results haven’t been great. But, until the past few months, the stock spent the vast majority of time in positive territory because I at least bought it when it was relatively cheap. Buying a pharma stock when it’s cheap usually limits the downside while one waits for a breakout product.

Basically, what I’m saying here is that Pfizer stock, if it doesn’t work out over the next 5 years, probably won’t lose much, but, if it wins, the upside could be substantial, and this means overall there is a good risk/reward here.

Conclusion

I bought Pfizer stock a couple of months ago for around $27 per share with an approximate 1% portfolio weighting, which is my standard size. I think under $29 per share for medium-term investors it has a good risk/reward. My expectation is that within a couple of years, earnings will recover to around where they were pre-COVID, which should provide some stock price appreciation. Investors can collect the dividend while they wait for any potential further catalyst to arise.

[ad_2]