Wall Street’s sleuth of bears is growing

This story was originally published on TKer.co

Stocks kicked off the new year on a positive note, with the S&P 500 climbing 1.4% last week. The index is now up 8.9% from its October 12 closing low of 3,577.03 and down 18.8% from its January 3, 2022 closing high of 4,796.56.

Meanwhile, the market’s many bears got more company.

Michael Kantrowitz, the chief investment strategist at Piper Sandler, expects the S&P 500 to tumble to 3,225 by year end, Bloomberg reported on Wednesday. This call makes him the most bearish of Wall Street’s top stock market forecasters.

Byron Wien, the legendary former chief investment strategist at Morgan Stanley and current vice chairman at Blackstone, warned on Wednesday that financial markets could slide during the first half of the year before rallying again.

“Despite Fed tightening, the market reaches a bottom by mid-year and begins a recovery comparable to 2009,“ Wien wrote.

Will the bears be proven right this year? Maybe.

But the fact that so much of Wall Street is bearish may actually produce the opposite result.

“Wall Street is bearish,” Savita Subramanian, head of U.S. equity strategy at BofA, wrote on Wednesday. “This is bullish.“

Subramanian was referring to the contrarian signal from BofA’s proprietary “Sell Side Indicator,” which tracks average recommended allocation to stocks by U.S. sell-side strategists. While it doesn’t currently reflect “extreme bearishness,” it’s at a level that “suggests an expected price return of +16% over the next 12 months (~4400 for the S&P 500).”

Subramanian’s official target for the S&P 500 is 4,000, which is on the bearish end of Wall Street. Though she has warned against being out of the market at a time when the consensus expects lower prices.

Going into 2022, Wall Street was caught wrong-footed by being too bullish ahead of what became a historic bear market.

Will the consensus be right this time with their bearishness?

We’ll only know in hindsight.

We do however know that the stock market goes up in most years.

And longer term investors should remember the odds of generating a positive return improves for those who can put in the time.

Reviewing the macro crosscurrents 🔀

There were a few notable data points from last week to consider:

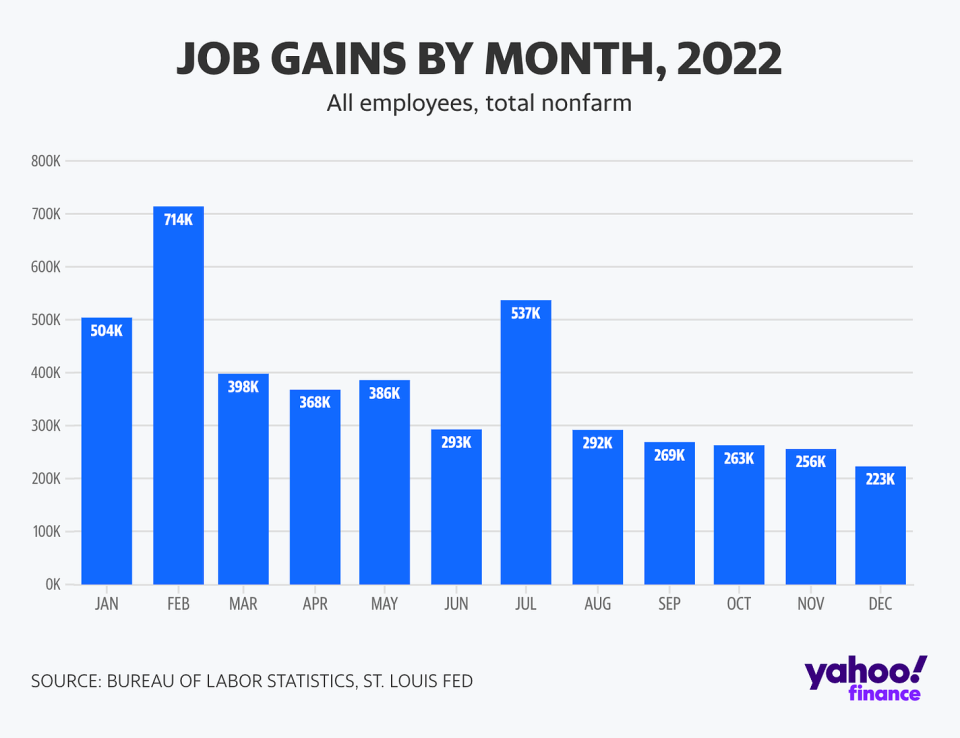

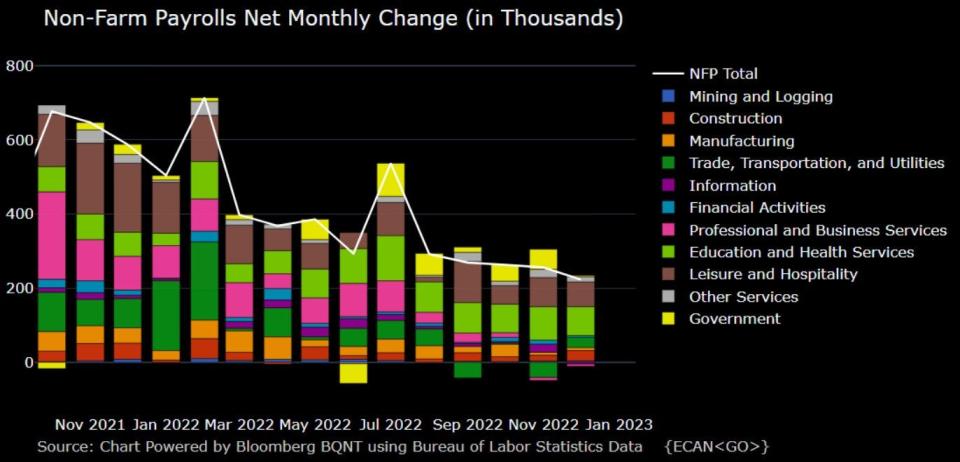

🚨 Job growth. According to BLS data released Friday, U.S. employers added 223,000 jobs in December, stronger than the 203,000 gain economists expected. Over the course of 2022, employers added a whopping 4.5 million jobs.

Almost all major industry categories reported gains. The information sector, which includes the tech industry, saw job losses. For more context on these losses, read: “Don’t be misled by no-context reports of big tech layoffs 🤨“

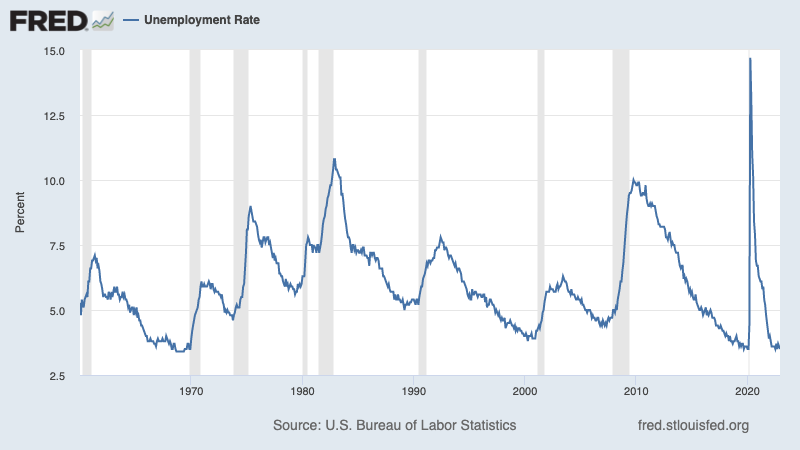

📉Unemployment rate tumbles. The unemployment rate fell to 3.5% (or 3.468% unrounded) from 3.6% in the prior month. This is the lowest rate since 1969.

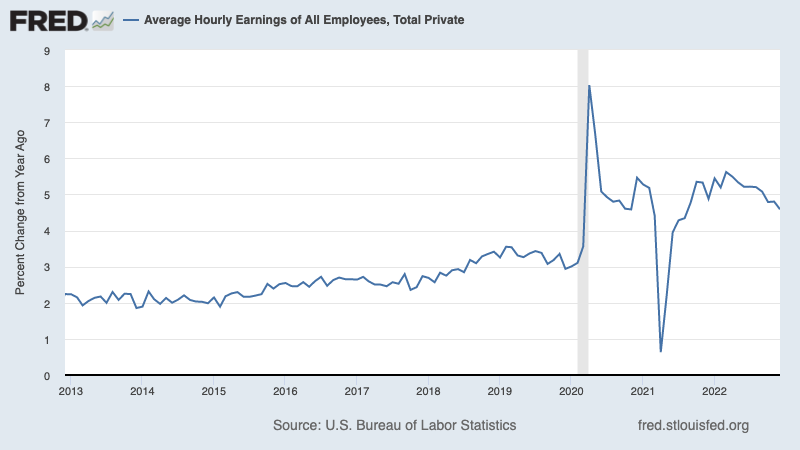

💰 Wage growth cools. Average hourly earnings in December increased by 0.3% month-over-month, cooler than the 0.4% rate expected. On a year-over-year basis, average hourly earnings were up 4.6%, which was lower than the 5.0% expected. For more on why this matters, read: “A key chart to watch as the Fed tightens monetary policy 📊“

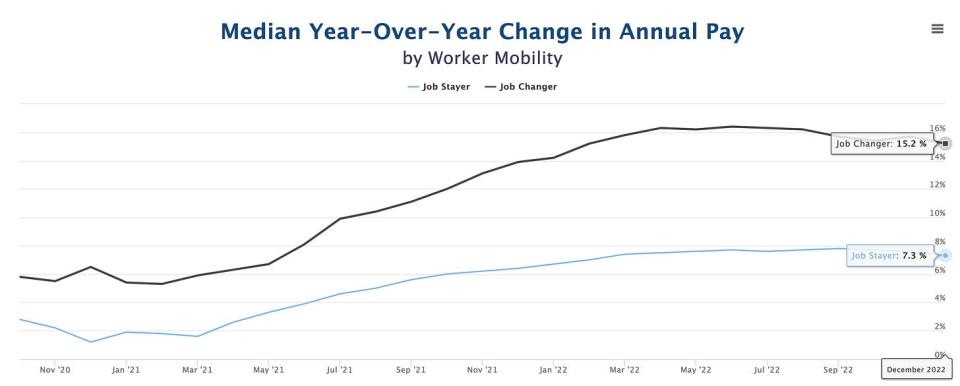

📈 Job switchers get better pay. According to ADP, which tracks private payrolls and employs a different methodology than the BLS, annual pay growth in December for people who changed jobs was up 15.2% from a year ago. For those who stayed at their job, pay growth was 7.3%.

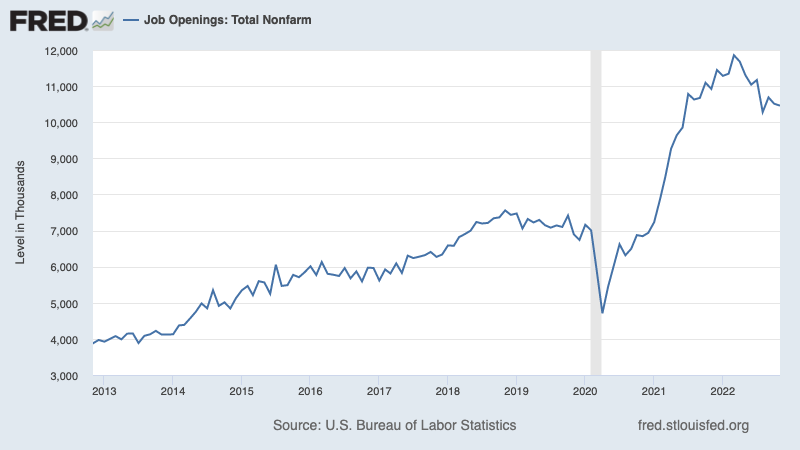

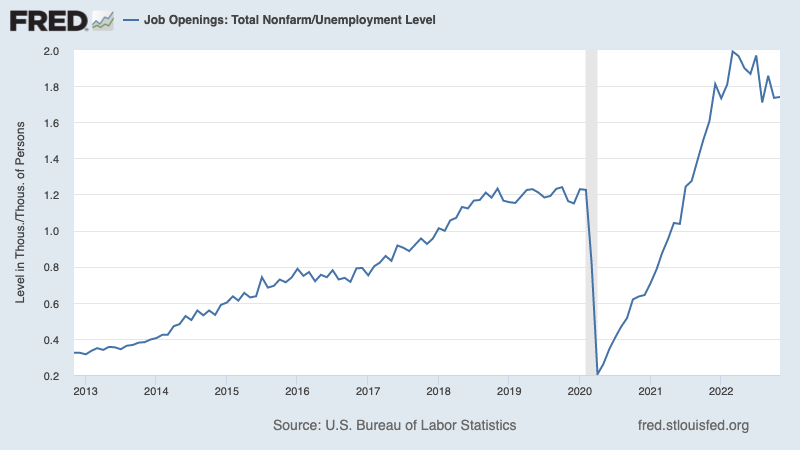

👍 There are lots of job openings. According to BLS data released Wednesday, U.S. employers had 10.46 million job openings listed in November, down modestly from 10.51 million openings in October. While openings are below the record high of 11.85 million in March, they remain well above pre-pandemic levels.

During the period, there were 6.01 million people unemployed. That means there were 1.74 job openings per unemployed person in November. This is down from 1.99 in March, but it still suggests there are lots of opportunities out there for job seekers.

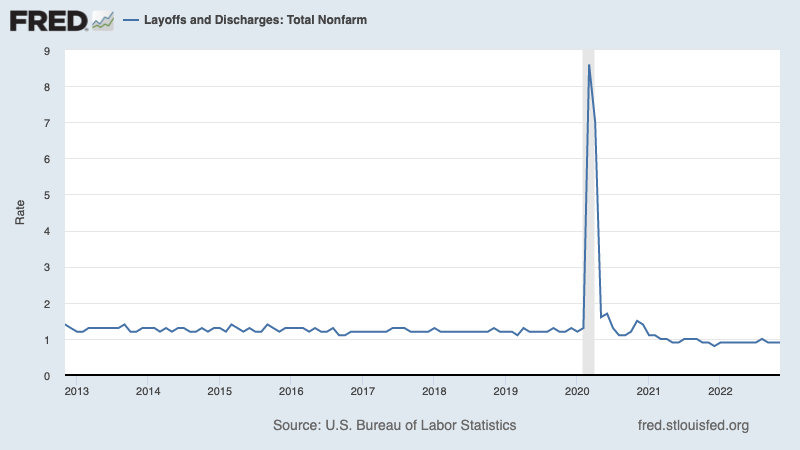

👍 Layoff activity is low. The layoff rate (i.e., layoffs as a percentage of total employment) stood at 0.9% in November, unchanged from its October level. It was the 21st straight month the rate was below its pre-pandemic lows.

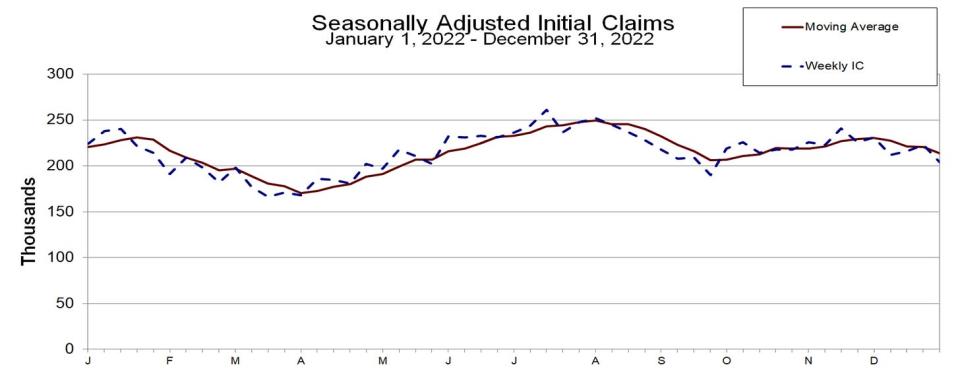

💼 Unemployment claims remain low. Initial claims for unemployment benefits fell to a three-month low of 204,000 during the week ending Dec. 31, down from 223,000 the week prior. While the number is up from its six-decade low of 166,000 in March, it remains near levels seen during periods of economic expansion.

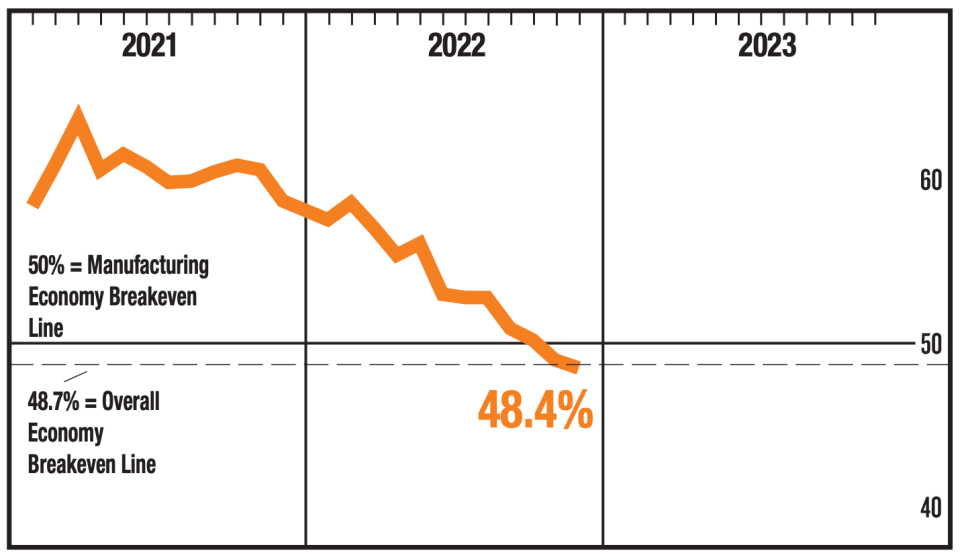

🛠 Manufacturing cools. The ISM’s Manufacturing PMI fell to 48.4 in December from 49.0 in November. A reading below 50 signals contraction in the sector.

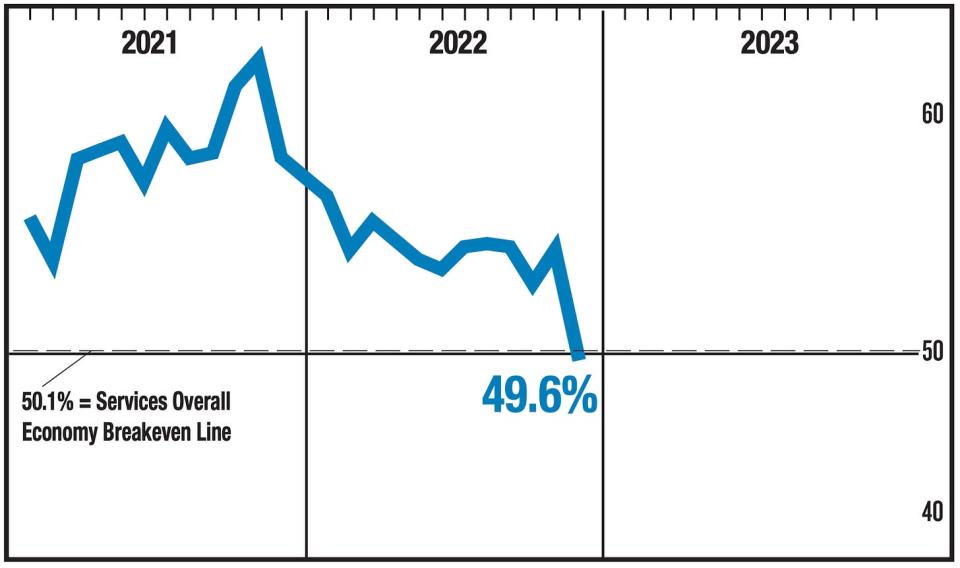

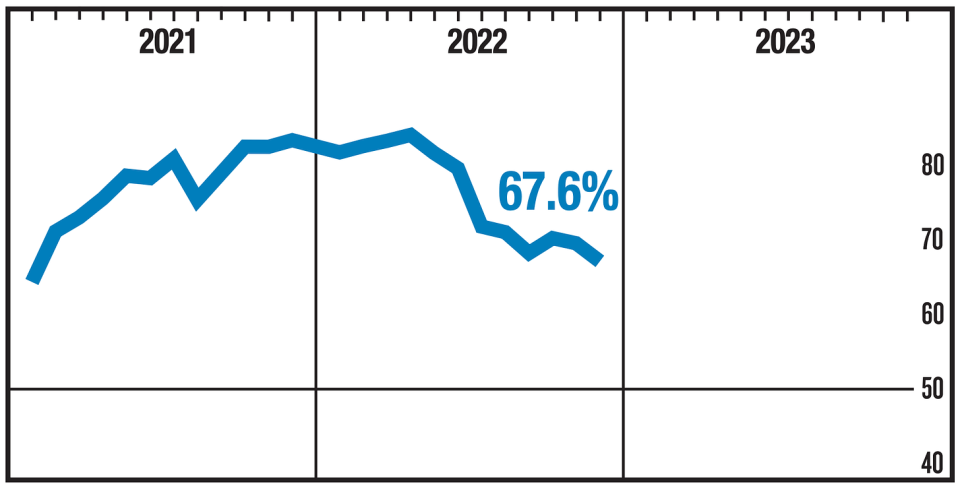

📉 Services cool. The ISM’s Services PMI fell to 49.6 in December from 56.5 in November. A reading below 50 signals contraction in the sector.

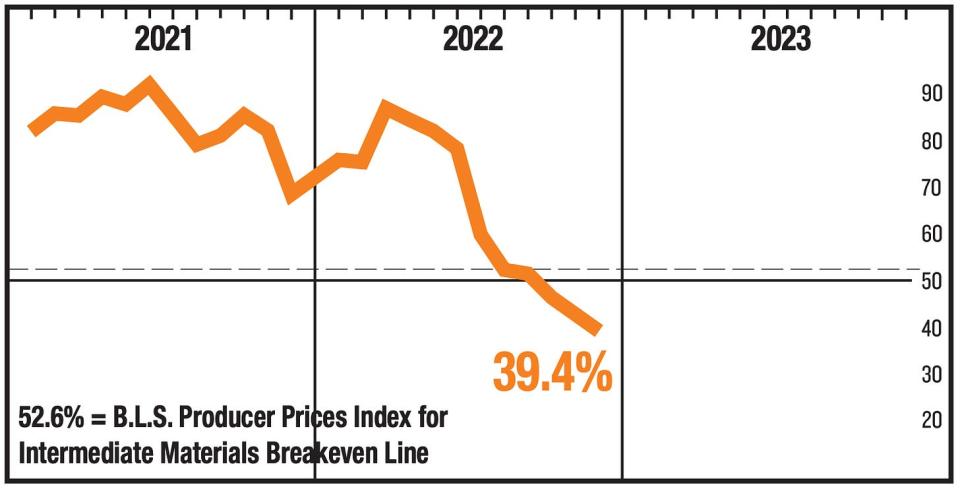

📉 Surveys say prices are cooling. ISM Manufacturing PMI Prices Index fell deeper into contraction.

The ISM Services PMI Prices Index suggests prices are still rising, but at a decelerating rate.

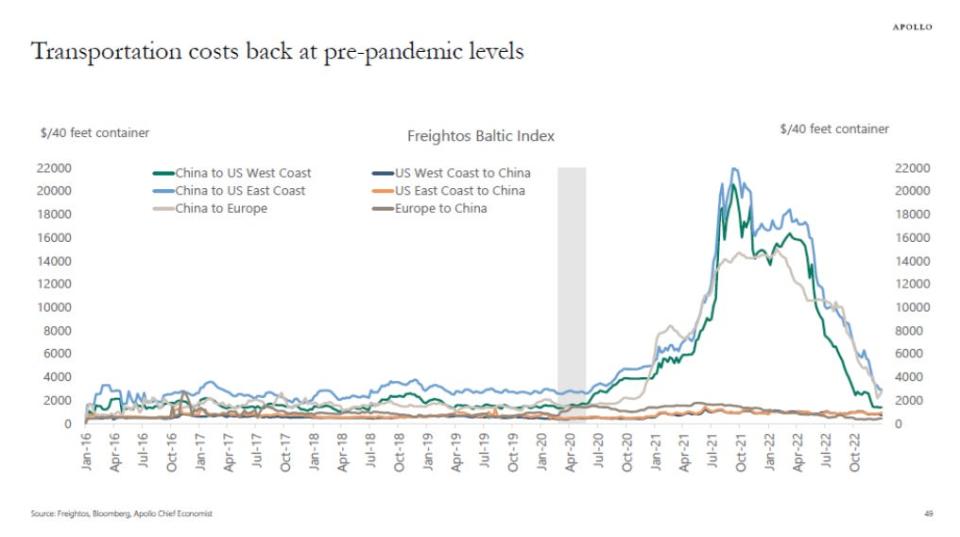

⛓️ “Supply chains are back to normal.” From Apollo Global’s chief economist Torsten Slok: “Supply chains are back to normal, and the price of transporting a 40-feet container from China to the US West Coast has declined from $20,000 in September 2021 to $1,382 today, see chart below. This normalization in transportation costs is a significant drag on goods inflation over the coming months.“

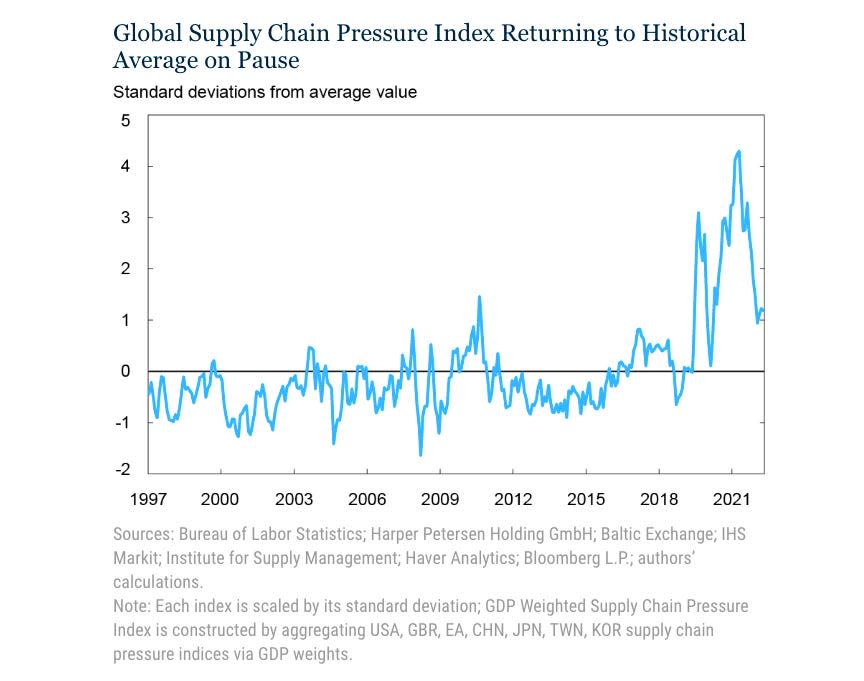

The New York Fed’s Global Supply Chain Pressure Index — a composite of various supply chain indicators — declined slightly in December and is hovering at levels seen in late 2020. From the NY Fed: “Global supply chain pressures decreased moderately in December, disrupting the upward trend seen over the previous two months. The largest contributing factors to supply chain pressures were rises in Korean delivery times and Taiwanese inventories, but these were more than offset by smaller negative contributions over a larger set of factors.“

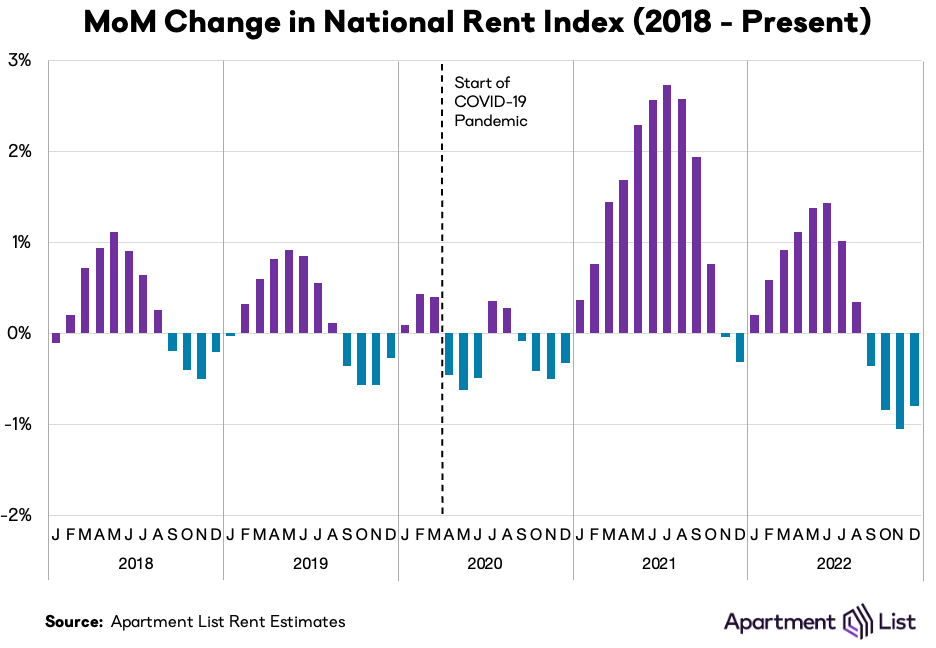

📉 Rents are down. From Apartment List: “We estimate that the national median rent fell by 0.8 percent month-over-month in December. This is the fourth consecutive monthly decline, and the third largest monthly decline in the history of our estimates, which start in January 2017. The preceding two months (October and November 2022) are the only two months with sharper declines.“

➕ No more negative yielding debt. From Bloomberg: “The world’s pile of negative-yielding debt has vanished, as Japanese bonds finally joined global peers in offering zero or positive income. The global stock of bonds where investors received sub-zero yields peaked at $18.4 trillion in late 2020, according to Bloomberg’s Global Aggregate Index of the debt, when central banks worldwide were keeping rates at or below zero and buying bonds to ensure yields were repressed.“

Putting it all together 🤔

Inflation is cooling from peak levels. Nevertheless, inflation remains high and must cool by a lot more before anyone is comfortable with price levels. So we should expect the Federal Reserve to continue to tighten monetary policy, which means tighter financial conditions (e.g. higher interest rates, tighter lending standards, and lower stock valuations). All of this means the market beatings will continue and the risk the economy sinks into a recession will intensify.

But it’s important to remember that while recession risks are elevated, consumers are coming from a very strong financial position. Unemployed people are getting jobs. Those with jobs are getting raises. And many still have excess savings to tap into. Indeed, strong spending data confirms this financial resilience. So it’s too early to sound the alarm from a consumption perspective.

At this point, any downturn is unlikely to turn into economic calamity given that the financial health of consumers and businesses remains very strong.

As always, long-term investors should remember that recessions and bear markets are just part of the deal when you enter the stock market with the aim of generating long-term returns. While markets have had a terrible year, the long-run outlook for stocks remains positive.

For more on how the macro story is evolving, check out the previous TKer macro crosscurrents »

For more on why this is an unusually unfavorable environment for the stock market, read “The market beatings will continue until inflation improves 🥊“ »

For a closer look at where we are and how we got here, read “The complicated mess of the markets and economy, explained 🧩”

This story was originally published on TKer.co

Sam Ro is the founder of TKer.co. Follow him on Twitter at @SamRo

Click here for the latest stock market news and in-depth analysis, including events that move stocks

Read the latest financial and business news from Yahoo Finance

Download the Yahoo Finance app for Apple or Android

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, and YouTube